The Reality of SMR Timelines for AI Data Centers: A Veteran’s View

- Tony Grayson

- Nov 21, 2025

- 11 min read

Updated: Feb 22

By Tony Grayson | Independent Strategic Advisor | Top 10 Data Center Influencer | Former CO USS Providence (SSN-719) | DOE/Naval Reactors Nuclear Certified | Advisory Board: TerraPower & Holtec International

Published: November 21, 2025 | Updated: February 22, 2026 | Verified: February 22, 2026

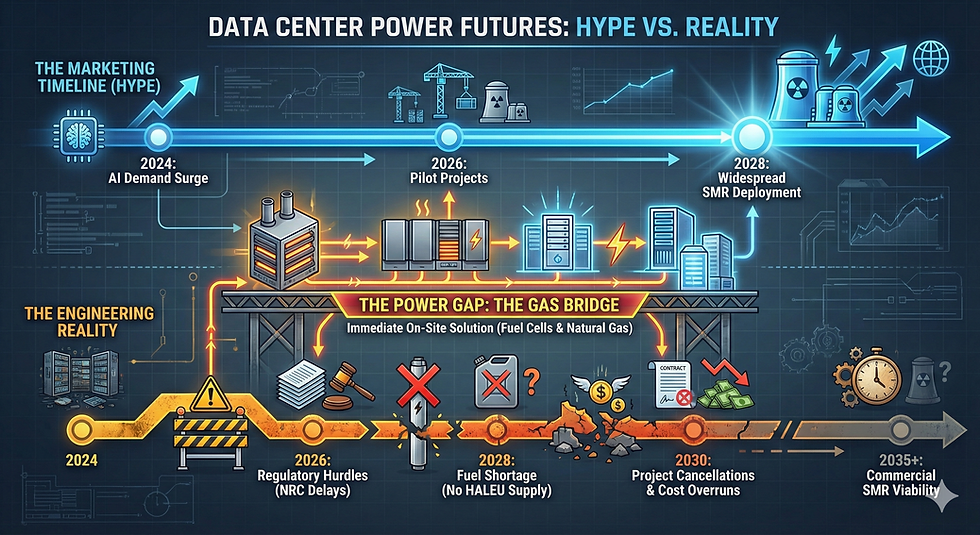

TL;DR — The Honest Nuclear Calendar

2025–2029: Reactor restarts only (Three Mile Island, Palisades). Feasible, limited supply.

2030–2035: Gen III+ large reactors and first commercial SMRs — if HALEU fuel scales and NRC licensing holds.

2035–2045: Advanced Gen IV SMRs at factory scale. This is when the marketing catches up to reality.

What to do now: Secure grid interconnection queue positions. Bridge with gas using Design for the Swap engineering. Sign PPAs with existing nuclear fleet operators. SMRs will not solve your 2028 AI power problem.

— Tony Grayson, DOE/Naval Reactors Nuclear Certified | TerraPower & Holtec International Advisory Boards

COMMANDER'S INTENT:

I have operated nuclear reactors since age 21. I advise TerraPower and Holtec International today. I know the difference between a PowerPoint reactor and a commissioned plant. The nuclear marketing wave is setting the industry up for a credibility crisis — because GPUs move in 3-year cycles, and reactors move in decades. This is the honest calendar.

— Tony Grayson, Commander (Ret.), USS Providence (SSN-719) | DOE/Naval Reactors Certified | TerraPower & Holtec Advisory Boards

If you’ve been following the recent nuclear boom, you’ve seen the headlines: Amazon commits to 5 GW. Google signs for advanced reactors. Oracle announces gigawatt-scale campuses. The message is clear: nuclear is the solution.

There is just one problem: GPUs move in 3-year cycles. Reactors move in decades.

I spent my early career commanding nuclear submarines, where "downtime" wasn't a metric; it was a mission failure. Later, I built data center infrastructure for Oracle, AWS, and Meta. I know the difference between a PowerPoint slide and a commissioned plant. I know what it takes to cool a reactor core versus a Blackwell rack.

While nuclear is the safest, most reliable generation method, the current wave of marketing is setting the industry up for a credibility crisis.

Below is the reality check on SMR timelines for AI data centers, HALEU fuel shortages, and what infrastructure buyers should actually do.

"GPUs move in 3-year cycles. Reactors move in decades. The current wave of nuclear marketing is setting the industry up for a credibility crisis."

— Tony Grayson, Former Commander, USS Providence (SSN-719) | TerraPower & Holtec International Advisory Boards

Key Concepts

Small Modular Reactor (SMR): Nuclear reactors under 300 MWe designed for factory fabrication and modular deployment. Examples: NuScale VOYGR (77 MWe), TerraPower Natrium (345 MWe), X-energy Xe-100 (80 MWe). Commercial availability at scale: 2032–2035.

HALEU: High-Assay Low-Enriched Uranium — enriched to 5-20% U-235. Required by most advanced Gen IV SMR designs. The U.S. has no domestic production at scale. The supply chain that doesn't exist yet.

Virtual PPA: A Power Purchase Agreement that is a financial hedge — it supports nuclear power on the grid but does not guarantee a physical wire from reactor to server rack. Most hyperscaler nuclear announcements are virtual PPAs.

Behind-the-Meter: Direct physical connection from a power source to your data center, bypassing the utility grid. Requires NRC co-location approval for nuclear. Extremely rare — not what most "nuclear data center" announcements describe.

Generation IV Reactor: Advanced nuclear reactor designs offering improved safety and efficiency profiles. Most require HALEU fuel. First factory-fabricated units expected post-2035.

Mankala Model: Cooperative cost-sharing structure where participants fund reactor construction and receive proportional power output — not just financial returns. The structure required if you want SMRs by 2035.

SMR Timelines for AI Data Centers: The Executive Summary

To optimize for decision-making, we must look at the specific delivery windows. Here is the realistic availability for nuclear power sources.

Near-Term (2025–2029): Reactor Restarts

Status: Feasible but limited.

Timeline: 3–5 years.

Examples: Palisades (Michigan) or Three Mile Island Unit 1.

Constraint: These require existing sites in good condition with willing local stakeholders.

Medium-Term (2030–2035): Gen III+ Large Reactors

Status: Proven technology, difficult execution.

Timeline: 10–14 years.

Constraint: The Vogtle Units 3 & 4 (AP1000) proved that even "off-the-shelf" designs can take a decade and cost $30B+.

Long-Term (2035–2045): Advanced SMRs (Gen IV)

Status: Experimental supply chain.

Timeline: Factory scaling likely post-2035.

Constraint: HALEU fuel availability and lack of factory fabrication lines.

If your strategy relies on SMR timelines for AI data centers intersecting with your 2028 capacity needs, you are missing the target.

A Note on the Nuclear Consensus

The consensus in 2024-2025 is that nuclear will solve the AI power crisis. Amazon, Google, Microsoft, and Oracle have all made nuclear announcements. The coverage is overwhelmingly bullish. The pressure on infrastructure executives to "have a nuclear strategy" is real.

Tony Grayson's position: the consensus is directionally correct and temporally wrong.

Nuclear is the right long-term answer. The physics are unambiguous: 90%+ capacity factor, carbon-free, baseload power that matches AI's always-on requirements. No other energy source comes close on reliability.

But the timeline is not 2028. The HALEU supply chain doesn't exist at scale. The NRC licensing pipeline is measured in years, not months. The factory fabrication lines for modular construction haven't been built yet.

Buying a nuclear PPA in 2024 does not put electrons in your server rack in 2028. It puts a financial instrument on your balance sheet and, eventually, power on the grid your data center also uses.

The operators who will win: those who acknowledge the timeline honestly, bridge intelligently with gas, secure grid positions now, and have the patience to capture nuclear's advantages when the supply chain actually matures.

The HALEU Fuel Gap: The Supply Chain That Doesn't Exist

The biggest risk to the "Advanced Nuclear" narrative is not the reactor; it is the fuel.

Many Gen IV designs (like TerraPower’s Natrium) require HALEU (High-Assay Low-Enriched Uranium).

The Demand: The DOE projects we need >40 metric tons by 2030.

The Supply: Current U.S. capacity is negligible (less than 1 ton/year).

The Problem: Prior to 2022, Russia was the primary commercial supplier.

Until domestic enrichment scales, a process that involves centrifuges, licensing, and billions in CAPEX...Gen IV SMRs have no fuel.

"If a vendor pitches you a 2030 SMR delivery date, ask one question: Where is your HALEU coming from? If they say 'the spot market,' they are gambling with your timeline and your capital."

— Tony Grayson, Top 10 Data Center Influencer | DOE/Naval Reactors Nuclear Certified

Regulatory Reality: The NRC Is Rigorous, Not Fast

Startups often promise "streamlined licensing." As a former operator, I can tell you that "fast" nuclear regulation is a myth you don't want to test. In the Navy, we had a saying: The specifications are written in blood. The NRC operates with a similar mindset.

The NRC licensing process generally follows three sequential steps:

Design Certification: 3–5 years.

Site License: 3–5 years.

Construction: 3–5 years.

While the Part 53 rule change aims to modernize this, we have yet to see a factory-fabricated reactor licensed and built in the U.S. under these new timelines.

The Bottom Line:

Small modular reactors represent genuine innovation, but they won't solve the AI energy crunch of 2028. If you are an infrastructure VP or CIO, you need to move beyond the press release.

1. Don't Just Buy Power; Buy the Order Book. A PPA isn't enough to move the needle on manufacturing. If you want SMRs in 2035, you need to participate in project equity or "Mankala model" structures (cooperative cost-sharing) today. You must fund the factory, not just the electrons.

2. Audit the Fuel Supply Chain. If a vendor pitches you a 2030 delivery date, ask one question: "Where is your HALEU coming from?" If they say "the spot market" or "DOE stockpiles," they are gambling with your timeline.

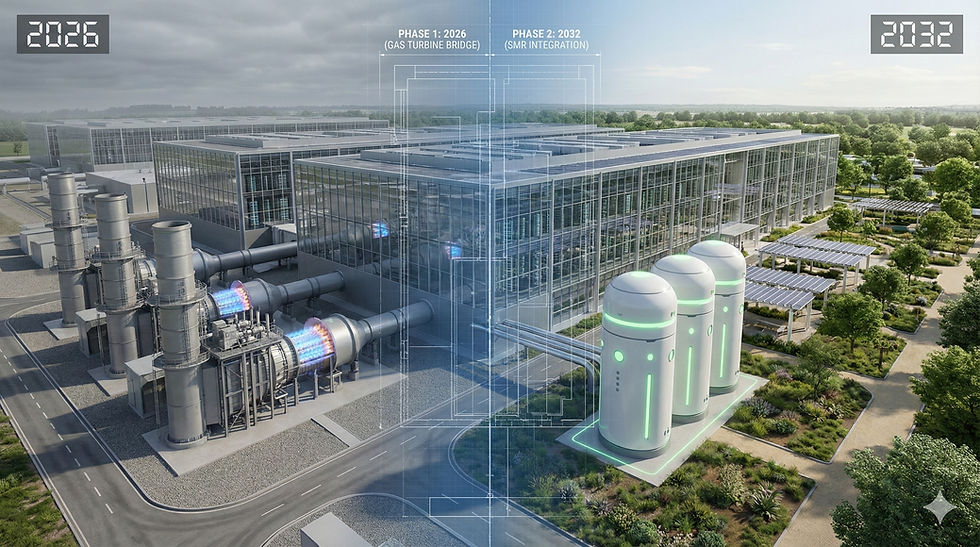

3. Bridge the Gap with Gas. For the next 7-10 years, the only scalable, dispatchable baseload that can support gigawatt-scale AI campuses is natural gas with carbon capture readiness. It’s not the answer we want, but it’s the answer physics dictates.

Let's build the future, but let's be honest about the calendar.

Recommended Viewing

For a deep dive into the specific challenges of integrating SMRs with industrial applications, this discussion from the OECD Nuclear Energy Agency is essential.

Frequently Asked Questions: Nuclear Power for AI Data Centers

When will SMRs be ready for AI data centers?

Realistically, commercial-scale SMR timelines for AI data centers point to 2032–2035 for the first wave of meaningful deployment. Pilot projects may appear sooner (late 2020s), but gigawatt-scale availability will lag behind current AI power demands. TerraPower's Natrium broke ground in Wyoming in June 2024 but won't achieve commercial operation until the early 2030s. NuScale received the first-ever SMR design certification in 2023 but cancelled its Utah UAMPS project due to cost overruns. The gap between announcement and electrons is measured in years, not months.

What is the difference between a PPA and a direct nuclear connection?

Most hyperscaler nuclear announcements are "virtual" PPAs (Power Purchase Agreements)—financial hedges that support the grid but do not guarantee a physical wire from the reactor to your server rack. You are still subject to local transmission interconnection queues, which can take 5+ years in congested markets. A direct connection (behind-the-meter) provides dedicated power but requires NRC co-location approval and is extremely rare. When Microsoft announces a "nuclear-powered data center," they're likely buying financial instruments, not building reactors next to servers.

What is HALEU fuel and why does it matter for SMRs?

HALEU (High-Assay Low-Enriched Uranium) is enriched to 5-20% U-235, required by many advanced SMR designs including TerraPower Natrium, X-energy Xe-100, and Kairos Power. The U.S. currently has no domestic HALEU production at scale—most supply came from Russian down-blending until 2024 sanctions cut off that source. Centrus Energy's Piketon facility is the only U.S. producer, operating at demonstration scale. This creates a multi-year supply chain bottleneck that delays SMR deployment regardless of how fast reactors get licensed.

Why are nuclear restarts faster than new SMR builds?

Restarting shuttered nuclear plants like Three Mile Island or Palisades uses existing NRC licenses, grid interconnections, trained workforce, and proven reactor designs with decades of operating history. New SMR builds require fresh NRC licensing (3-5 years minimum), first-of-a-kind engineering validation, new fuel supply chains (especially HALEU), and greenfield construction with no learning curve. Constellation's Crane Clean Energy Center (TMI restart) targets 2028—years ahead of any commercial SMR. Holtec's Palisades restart follows similar logic.

Can we use existing nuclear waste as fuel for SMRs?

Some Gen IV designs promise to consume spent fuel through reprocessing, but this technology faces significant policy hurdles in the United States. The Nuclear Waste Policy Act and proliferation concerns have blocked commercial reprocessing since the Carter administration banned it in 1977. While France and Russia reprocess spent fuel commercially, the U.S. has no infrastructure for this approach. It is not a commercial option for near-term data center power—don't let marketing materials convince you otherwise.

What should data center operators do while waiting for SMRs?

Focus on grid interconnection queue positions now—these take 5+ years in congested markets. Pursue natural gas bridge strategies with "Design for the Swap" engineering that allows future nuclear integration. Secure PPAs with existing nuclear fleet operators like Constellation, Duke, and Southern Company. Monitor restart projects like Crane Clean Energy Center and Palisades. SMRs are a 2032+ solution—current AI demand requires power today. The operators who secure grid positions and existing nuclear PPAs now will have competitive advantages when SMRs eventually arrive.

What is the NRC licensing timeline for new SMRs?

The NRC licensing process for new reactor designs takes 3-5+ years minimum for design certification alone. NuScale received the first-ever SMR design certification in January 2023 after a 6-year review that began in 2017. Combined Construction and Operating License (COL) applications add additional years before construction can begin. TerraPower Natrium, X-energy Xe-100, and Kairos Power are still working through the pipeline. The ADVANCE Act (2024) aims to streamline NRC processes, but regulatory acceleration takes years to implement.

How much power can SMRs provide to data centers?

Individual SMR modules range from 50-300 MWe depending on design. NuScale's VOYGR is 77 MWe per module (up to 12 modules = 924 MWe per plant). TerraPower Natrium is 345 MWe with 500 MWe peak using molten salt storage. X-energy Xe-100 is 80 MWe per module. For context, a hyperscale AI data center campus may require 500 MW to 2+ GW—Meta's Louisiana campus will exceed 1 GW. Multiple SMR modules or plants would be needed, requiring billions in capital and multi-year construction timelines per site.

What is the Microsoft-Constellation Three Mile Island deal?

In September 2024, Microsoft announced a 20-year PPA with Constellation Energy to restart Three Mile Island Unit 1 (renamed Crane Clean Energy Center). This 835 MW reactor—shut down in 2019 for economic reasons, not safety—will provide carbon-free power to the PJM grid supporting Microsoft's data centers. This is a restart of an existing, proven pressurized water reactor, not an SMR. It demonstrates that restarting existing nuclear plants is faster and lower-risk than waiting for Gen IV designs that have never operated commercially.

Why is nuclear baseload power valuable for AI data centers?

Nuclear provides 24/7 carbon-free baseload power at 90%+ capacity factors—the highest of any energy source. AI training clusters running NVIDIA GB200 or AMD MI300X require constant power; you can't pause a training run when the wind stops. Intermittent renewables require battery storage (expensive, fire risk) or natural gas backup (carbon emissions). Nuclear's reliability matches AI's always-on compute requirements, which is why hyperscalers are pursuing nuclear PPAs despite 2030s timelines. The alternative is curtailing AI workloads during grid stress events.

What are microreactors and when will they be available?

Microreactors are very small nuclear reactors (1-20 MWe) designed for remote locations, military bases, or distributed power. Examples include Project Pele (DoD transportable reactor), Westinghouse eVinci, and Oklo Aurora. While promising for edge data centers, mining operations, or military forward operating bases, they face the same NRC licensing bottlenecks as larger SMRs. Project Pele completed a prototype in 2024, but commercial deployments are unlikely before 2030. Don't plan your edge computing strategy around microreactor availability.

Who is Tony Grayson and why is he qualified to write about nuclear for data centers?

Tony Grayson commanded nuclear submarine USS Providence (SSN-719) with DOE/Naval Reactors certification from Admiral Rickover's program — operating reactors from age 21. He serves on advisory boards for TerraPower (Bill Gates' nuclear company building Natrium) and Holtec International (pursuing Palisades restart). He previously led data center infrastructure at Oracle ($1.3B budget, 35+ cloud regions), Meta (30+ data centers), and AWS — giving him unique insight into both nuclear operations and hyperscale power demands. More at tonygrayson.ai

What is Sam Altman's nuclear energy strategy and how does it affect AI infrastructure?

Sam Altman has invested in Oklo, a microreactor company pursuing NRC licensing for its Aurora fission reactor, and has backed other nuclear ventures. OpenAI's power demands for training frontier models require gigawatt-scale continuous power — the same physics problem every major AI lab faces. The challenge: Oklo's Aurora faces the same HALEU bottlenecks and NRC licensing timelines as larger SMRs. Altman's nuclear investments are directionally correct but operationally years away from solving current power constraints.

What are Google and Amazon doing with nuclear energy for their data centers?

Google signed a PPA with Kairos Power in October 2024 for 500 MW of advanced nuclear power, targeting first delivery in 2030 with full capacity by 2035. Amazon Web Services signed agreements supporting nuclear projects including the Talen Energy nuclear campus in Pennsylvania, and invested in X-energy Xe-100 reactors. Both are PPAs — financial agreements supporting nuclear power on the grid, not direct reactor-to-server connections. The carbon accounting benefits arrive before the physical power does.

"Bridge the gap with gas — and design for the swap. Build it so nuclear can plug in later without tearing out the walls. That's not a compromise. That's physics-first planning."

— Tony Grayson, Independent Strategic Advisor | Former SVP Oracle, AWS, Meta

Related Reading from Tony Grayson:

The SMR Market Correction: Why the AI Infrastructure Timeline Requires a Gas-to-Nuclear Bridge — The companion post on Design for the Swap strategy

From Parameters to Physics: Why Watts per Token is the Only Metric for Industrial AI — Power physics vs. benchmark competition

Is AI Infrastructure Overbuilt? An Operator's View on the $100B Gamble — The Kemper Trap applied to AI CapEx

Training vs. Inference: The $300B AI Shift Everyone is Missing — Why nuclear baseload matters more for inference than training

Sources & Further Reading

____________________________________

Tony Grayson is an independent strategic advisor and recognized Top 10 Data Center Influencer.

A former U.S. Navy Submarine Commander with DOE/Naval Reactors nuclear certification and recipient of the VADM Stockdale Award for Inspirational Leadership, Tony commanded USS Providence (SSN-719) and operated nuclear reactors from age 21. He serves on advisory boards for TerraPower and Holtec International, and previously led global infrastructure as SVP at Oracle ($1.3B budget), AWS, and Meta.

He serves as Veterans Chair for Infrastructure Masons and advises independently on AI infrastructure, nuclear energy, and defense technology.

Read more at tonygrayson.ai

Comments